Determining how much home you can actually afford goes beyond the list price of a property. Other factors that will affect your monthly payment include interest rates, taxes, insurance, income, debt, and future monthly expenses - to name just a few. While there are numerous “affordability” calculators out there, it’s important to first understand the whole picture.

Before you buy, take action to determine how much home you can afford.

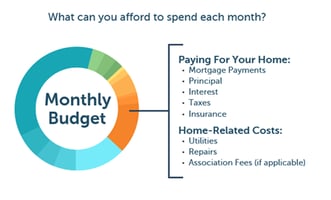

Assess your financial readiness to determine what you can afford – both in terms of monthly housing-related costs and total cost of a home. Examine your monthly income and spending habits, and determine how much you can afford to spend, including mortgage payments and home-related costs.

Assess your financial readiness to determine what you can afford – both in terms of monthly housing-related costs and total cost of a home. Examine your monthly income and spending habits, and determine how much you can afford to spend, including mortgage payments and home-related costs.

Before you apply for a mortgage, you should know approximately how much home you may be able to afford. First, do you have any savings or money that you are able to put towards a down payment? Homebuyers commonly put between 5 and 20% of the total cost of the home as a down payment. While lenders will ultimately determine the size of loan for which you qualify, you can still get an idea about an affordability range – this number can help inform your home search. One estimate is that borrowers can generally afford a mortgage that equals two to three times their annual household income. The amount you are able to put down, plus the amount of your mortgage, can give you a sense of the total cost of a home you can afford.

Factors That Lenders Consider When Determining The Terms of the Loan

In addition to understanding about how much you can afford, it is important to know some of the factors that lenders consider when determining the terms of the loan for which you may qualify. Most lenders will judge your loan worthiness in four general ways - these are sometimes called the “Four Cs” of loan and credit. We’ll explore some important calculations related to the “Four Cs” so you can better understand how lenders review your financial history and determine your mortgage amount.

Capacity

One of the calculations that lenders use to determine the amount of your loan is your debt-to-income ratio, or DTI. This is part of the “capacity” assessment of the “Four Cs.” Your DTI compares your monthly debt payments to your monthly income, and gives a lender a sense of your ability to repay debt. In general, the lower your DTI, the better your balance between debt and income, and the more likely you’ll be approved to borrow. Many sources say that 43% is generally the highest DTI a borrower can have and still qualify for a mortgage.

To calculate your DTI, first determine your monthly income; you can do this by reviewing your paycheck or online deposit history, or dividing your annual gross income by 12. Then, determine your monthly debt expenses. These tend to be fixed costs that you pay each month. Finally, divide your monthly debt expenses by your monthly income. Even if you do not know the precise amount of your monthly income or debt, estimating your DTI is a helpful step in better understanding how potential lenders might evaluate your loan worthiness.

Credit

In addition to “capacity,” “credit” is another of the “Four Cs” that can have a big impact on your home buying journey. Lenders consider your credit score when determining whether to make a loan and the amount that a loan will be for. Your credit score is a three-digit numerical rating that reflects how likely you are to repay your debt. In general, the higher (or stronger) your credit score, the better the mortgage terms you may receive. The Fair Credit Reporting Act (FCRA) allows you to receive one free copy of your credit report each year from one of the nationwide credit reporting agencies. You can go to annualcreditreport.com to request your report today. As you review your credit report, you can plan or begin to take any necessary steps to start improving your credit score.

Deciding to buy a home is a big step, but it doesn’t have to be intimidating. Knowing the questions to ask and things you can do to get started will help you make the decision that is best for you! At Arbor Financial, we’re here to help you navigate this exciting time and will always be just a phone call or click away.